{kind=link}

Thank you for reading this post. This blog is published by our YouTube Channel, BRO. If you are looking for reliable, no B.S. ways to supplement your retirement income each month, check out the channel's course on Udemy. Remote Jobs for Retirees and Expats.

In the case of deciding when to take Social Safety advantagesthe query most individuals ask themselves is:

Is it higher to take Social Safety at 62 or 67?

This is without doubt one of the most vital choices you’ll make in your retirement years. It could possibly affect your month-to-month earnings for the remainder of your life — particularly given growing life expectations and the rising price of dwelling.

This text will assist you to consider the benefits and downsides of claiming Social Safety early at 62 versus ready till full retirement age at 67. We’ll additionally take a look at the non-public and monetary elements which will affect your choice.

What You Must Know About Social Safety Retirement Ages

Social Safety advantages permits you to start claiming retirement advantages as early as 62, however your profit quantity might be completely lowered in case you file earlier than your Full Retirement Age (FRA) — which, for most individuals at present, is 67. Conversely, in case you delay previous FRA as much as age 70, your advantages will develop much more.

Right here’s a fast abstract:

- 62 — Earliest claiming age, as much as a 30% everlasting profit discount.

- 67 — Full Retirement Age (FRA), you obtain 100% of your Major Insurance coverage Quantity.

- 70 — Newest claiming age for Social Safety; advantages improve 8% per yr delayed after FRA.

- For a customized estimate, use the SSA’s Social Safety Retirement Estimator.

Taking Social Safety at Age 62

✅ Benefits of Claiming at 62

- Earlier Earnings

Beginning at 62 provides you earlier entry to earnings. In case you want cash as a result of retirement, job loss, well being points, or different private circumstances, claiming at 62 can present monetary reduction. - Extra Whole Checks Acquired

Claiming at 62 as an alternative of 67 means receiving 60 additional month-to-month checks over 5 years. Even when every examine is smaller, the cumulative profit may stability out — particularly in case you don’t dwell previous your mid-70s. - Extra Time to Take pleasure in Retirement

Not everybody will dwell lengthy sufficient to see the so-called “break-even age” — the age at which the bigger checks you’d obtain at FRA or after would catch as much as the smaller checks you obtained beginning at 62. Taking your profit early might imply extra lively years throughout retirement.

❌ Disadvantages of Claiming at 62

- Everlasting Discount in Advantages

Claiming at 62 can cut back your profit by as much as 30%. For instance, in case your FRA profit is $2,000/month at 67, you may solely obtain round $1,400/month beginning at 62. That $600 distinction will final for all times. - Earnings Take a look at Reductions if Nonetheless Working

In case you plan to work whereas claiming earlier than FRA, Social Safety has an earnings check. In 2025, the restrict is roughly $22,320; each $2 earned above that restrict will cut back your profit by $1. Examine the SSA’s earnings check calculator for specifics. - Smaller Spousal & Survivor Advantages

Your Social Safety profit additionally impacts your partner or survivors. Claiming early lowers spousal and survivor advantages too — so when you have a lower-earning partner or somebody who is dependent upon your earnings, it is a massive issue to weigh.

Taking Social Safety at Age 67

✅ Benefits of Claiming at 67

- Full Month-to-month Profit

Claiming at your FRA (age 67 for most individuals now approaching retirement) means you obtain your full profit — 100% of what you earned over your working profession. - Larger Lifetime Advantages if You Reside Longer

Individuals who dwell into their mid-80s or past could obtain more cash over their lifetime by ready. Let’s take a look at a fast instance:

| Age Claimed | Month-to-month Profit | Whole Acquired by Age 85 |

| 62 | $1,400 | $386,400 |

| 67 | $2,000 | $432,000 |

By age 85, ready to assert at 67 might internet you almost $46,000 extra.

- Spousal and Survivor Advantages

By delaying, you additionally improve the profit quantity your surviving partner would obtain after your dying — which is very vital in the event that they depend on your profit as a part of their earnings.

❌ Disadvantages of Ready Till 67

- Delayed Earnings

In case you want earnings to cowl bills in your early 60s, delaying can require utilizing up financial savings, 401(ok)s, or different investments. That might expose you to market fluctuations and tax implications. - Unsure Well being or Life Expectancy

If in case you have well being points or a household historical past that means a shorter-than-average lifespan, delaying could imply fewer checks in complete. - Lacking Early Retirement Alternatives

If you wish to take pleasure in touring or new experiences earlier in retirement — whilst you’re bodily ready — you may worth receiving advantages at 62 greater than receiving the next month-to-month profit beginning at 67.

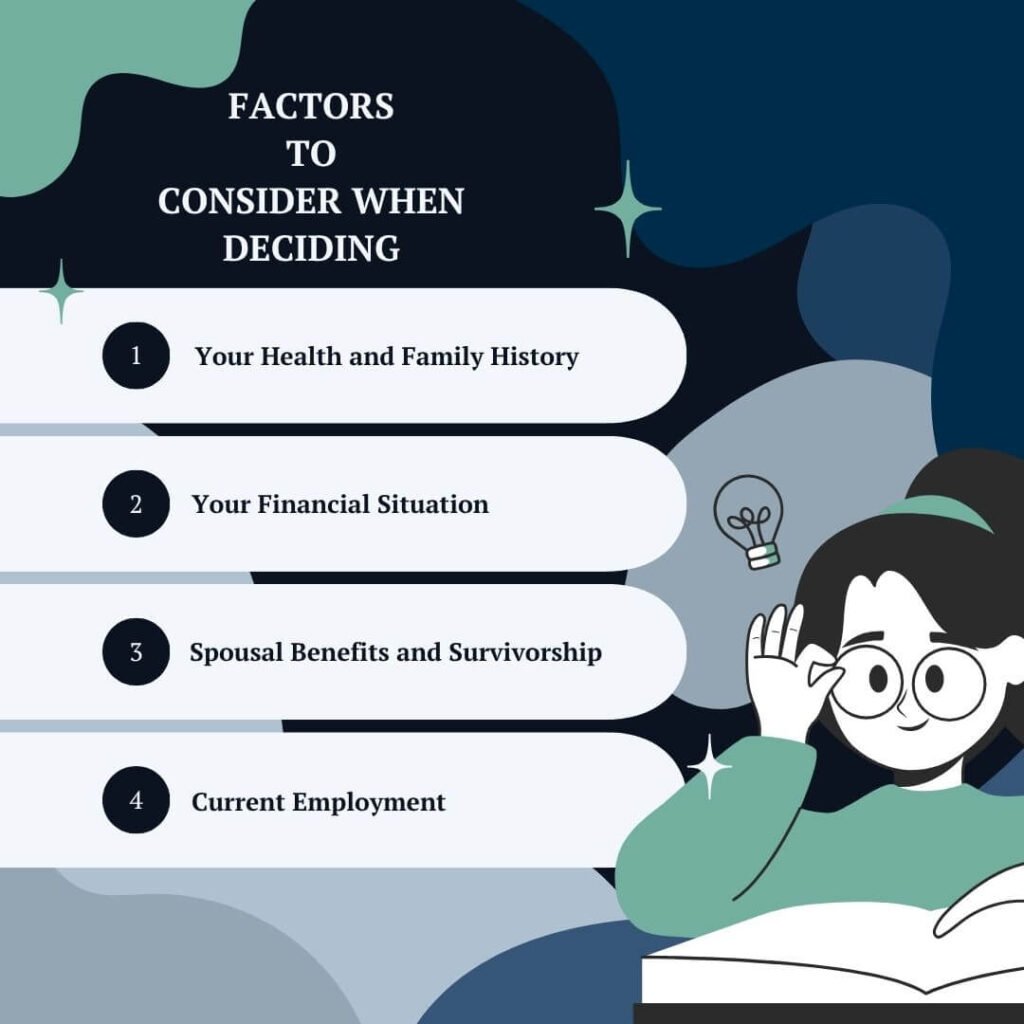

Components to Take into account When Deciding

1. Your Well being and Household Historical past

If in case you have good cause to imagine you’ll dwell into your mid-80s or past, ready might make monetary sense. Alternatively, when you have well being challenges, claiming at 62 could assist you to maximize the overall {dollars} you obtain.

2. Your Monetary Scenario

Do you want the earnings to dwell? In that case, claiming early might assist. However when you have financial savings and different earnings sources (pensions, investments), ready can develop your Social Safety profit — offering a bigger, inflation-adjusted earnings stream for later in retirement.

3. Spousal Advantages and Survivorship

In case you’re the higher-earning partner, delaying as much as FRA or 70 can improve the advantages obtainable to your surviving partner after you move.

4. Present Employment

In case you’re nonetheless working and incomes substantial earnings earlier than FRA, early claiming can cut back your profit because of the earnings check. Ready till FRA eliminates this concern.

Break-even Evaluation

A essential a part of deciding is calculating your break-even level — the age at which complete advantages obtained in case you wait will surpass what you’d obtain in case you claimed earlier.

Right here’s a simplified instance, assuming:

- Age-62 profit: $1,400/month

- Age-67 profit: $2,000/month

You’d obtain $84,000 ($1,400 x 60 months) within the 5 years between 62 and 67.

To make up that $84,000 distinction with a $600 greater month-to-month examine ($2,000 – $1,400), you’d want 140 months, or about 11.7 years.

Which means your break-even age can be roughly 78.7.

In case you dwell previous 79, ready pays off. If not, claiming earlier may yield extra complete {dollars}.

Inflation and COLA Affect

Social Safety advantages are inflation-adjusted by way of an annual Value-of-Dwelling Adjustment (COLA). Ready to take Social Safety advantages means receiving a bigger base quantity to develop with COLA yearly, which may matter enormously as you age and bills rise.

Actual-World Situations

Situation 1: Well being Issues

Mary, 61, just lately had a well being scare and doesn’t anticipate to dwell previous 75. Claiming at 62 gives her with earnings when she will take pleasure in it most and provides her probably the most cash throughout her shorter projected lifespan.

Situation 2: Sturdy Household Historical past of Longevity

Mark, additionally 61, comes from a long-lived household — most of his kinfolk dwell into their 90s. Ready till 67 and even 70 might lead to a a lot bigger profit that can assist him properly into his later years.

There’s no one-size-fits-all reply. The choice of whether or not to take Social Safety at 62 or 67 is extremely private. It is dependent upon your well being, monetary want, life expectancy, marital standing, and objectives for retirement.

In case you’re unsure which path to decide on, speak to a trusted monetary advisor or discover instruments just like the SSA’s Retirement Age Chart and different on-line calculators. They’ll assist you to mannequin completely different choices and choose what’s best for you.

And bear in mind — it is a everlasting alternative. Take your time, do your analysis, and be sure you really feel comfy earlier than claiming. Retirement is one in all life’s most rewarding chapters — you need to set your self up for probably the most safety and pleasure potential. vital factor is to plan fastidiously in order that whichever path you select matches your objectives for a safe and fulfilling retirement.

YOU CAN ALSO READ :

*Finest 15 Hobbies for Aged at Dwelling to Hold Them Busy and Glad

*Finest 10 Gown Code Concepts: What to Put on to A Retirement Get together?

*Finest Retirement Get together Decorations Concepts to Make It Memorable